Argentina Found Another Source of Dollars, but the Risk Did Not Disappear

Argentina Found Another Source of Dollars, but the Risk Did Not Disappear

Argentina Found Another Source of Dollars, but the Risk Did Not Disappear

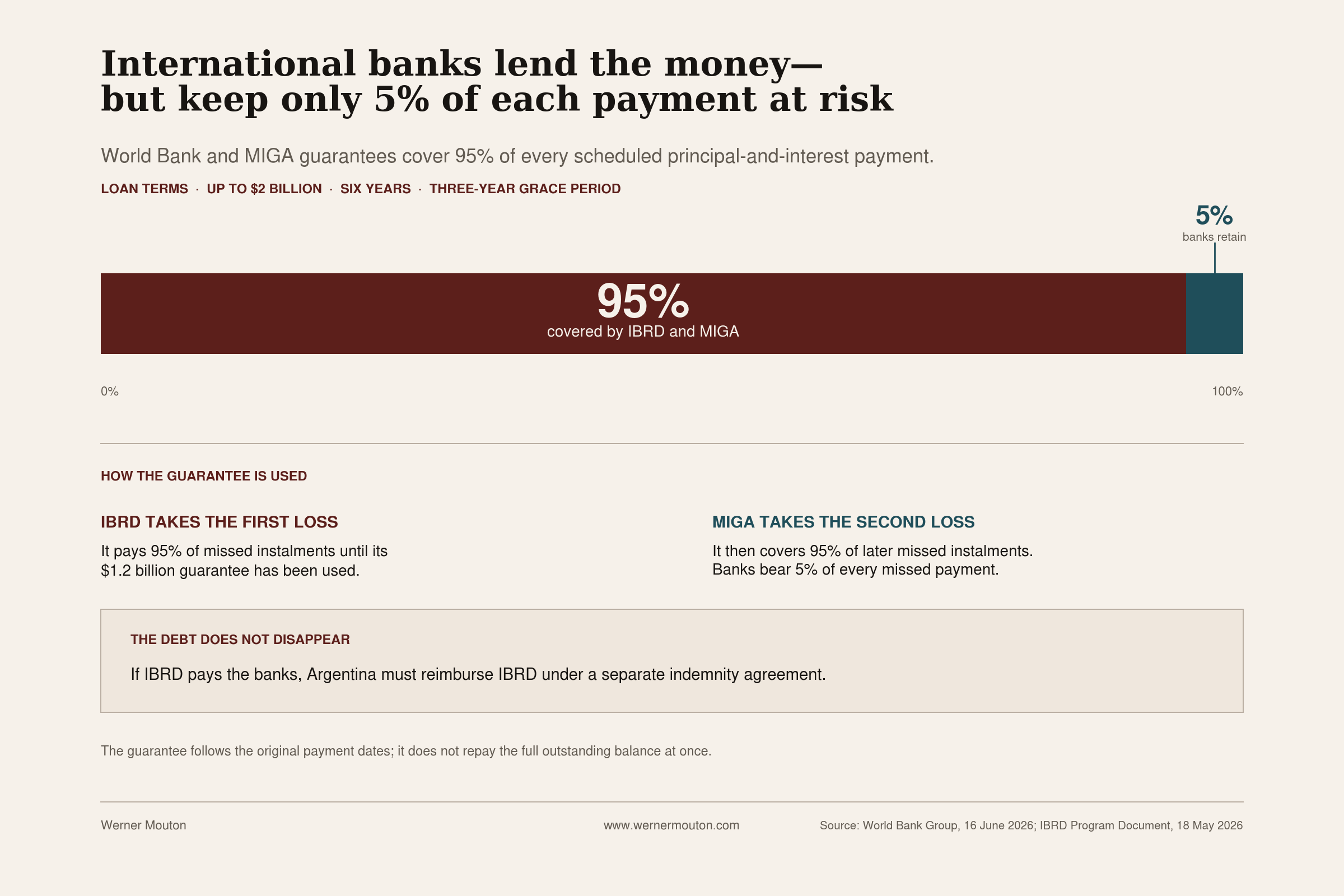

The World Bank-backed commercial loan can supply up to $2 billion without a new foreign-law bond. The banks provide the money, but they retain only 5 per cent of the risk on each payment.

Argentina can raise up to $2 billion from commercial banks because the World Bank and MIGA will cover 95 per cent of every scheduled payment.

Argentina can raise up to $2 billion

This deal supplies one answer to the question raised by Argentina’s $4.3 billion bond payment on 9 July. The government paid that bill without issuing a new bond abroad, but it still needed a plan for the bills that follow. A World Bank-backed bank loan now forms part of that plan.

The loan does not mark a normal return to world markets. Commercial banks will supply the dollars, but two parts of the World Bank Group will stand between those banks and Argentina. The International Bank for Reconstruction and Development, or IBRD, will take the first loss. The Multilateral Investment Guarantee Agency, or MIGA, will take the second.

The order matters. If Argentina misses a principal or interest payment, IBRD will pay the banks 95 per cent of the amount due. It will keep doing so on the original payment dates until its $1.2 billion guarantee has been used. MIGA will then cover 95 per cent of later missed payments. The banks will bear the remaining 5 per cent each time.

The banks therefore lend to Argentina, but they keep little direct Argentine risk. The World Bank’s talks with lenders found that banks preferred this combined cover. A guarantee from IBRD alone would have left them with more risk, raised the price and reduced the number willing to lend.

This helps explain why the government can raise commercial money without issuing a new foreign-law bond. The loan rests partly on Argentina’s promise to pay, but its price also rests on the balance sheets of IBRD and MIGA. The World Bank document calls the structure a bridge to full market access. A bridge connects two places. It is not the destination.

The form of the loan matters too. A foreign-law bond spreads the debt among many investors. This loan will most likely come from a club of banks that can negotiate the terms and price the guarantee directly. The World Bank chose to support a commercial loan rather than a bond because a small group of named lenders can manage the guarantee more precisely if Argentina misses a payment. Caputo can therefore avoid a new foreign-law bond while still borrowing from lenders abroad.

The guarantee also does not make Argentina’s debt disappear. If IBRD pays the banks, Argentina must reimburse IBRD under a separate agreement. The debt moves from one relationship to another. Argentina first owes the banks. If the guarantee is called, it owes IBRD for the amount IBRD paid.

Nor can the banks demand the full guaranteed balance from IBRD as soon as Argentina misses one payment. The guarantee follows the original payment schedule. It covers missed instalments as they fall due. Each payment also reduces the guarantee for good.

The structure gives Argentina something valuable: time. The commercial loan will run for six years and includes a three-year grace period. Argentina will pay interest during those first three years but will not repay principal. Without the package, the World Bank says the likely alternative would combine a direct $1.2 billion IBRD loan with $800 million in one-year commercial finance. That short loan would need to be replaced each year.

The six-year loan removes that annual test. It lowers interest costs during the years when Argentina faces its heaviest pressure and prevents another short-term maturity from joining the loans and repos already due in 2027.

But the World Bank document makes a careful distinction. Measured in today’s money, the guaranteed plan and the likely alternative cost broadly the same. The main gain comes from when Argentina pays and how often it must return to lenders. The package cuts near-term interest costs, delays principal payments and reduces the risk that a one-year loan becomes hard or expensive to replace.

That makes the deal useful, but it also defines its limits. Argentina has not proved that investors will fund it for six years without support. It has proved that banks will lend when the World Bank Group covers almost every dollar due to them.

The July bond payment showed that Argentina could find the dollars for one large bill. This package shows where as much as $2 billion of the next dollars may come from. The banks will provide them. The World Bank Group will carry most of the payment risk. Argentina will keep the final duty to pay.

The next test is whether this bridge leads to market access before Argentina needs another bridge.